*************** PEBBLEWRITER.COM IS LIVE! TO SIGN UP, CLICK HERE ***************

Tuesday, March 31, 2020

Charts I'm Watching: Mar 31, 2020

Futures are off slightly as we approach the open, recovering 25 points from the overnight lows as the algos resume control.

VIX continues to call the shots, as it has dropped through both the

red neckline and the SMA20. Yet, it continues to bounce every time

SPX/ES approach a breakout point, suggesting that the bounce might have completed.

For its part, SPX has yet to break above the purple trend line from 2016 and, like ES, avoided making a higher high yesterday.

As expected, USDJPY has edged back above its SMA200, providing an extra nudge for stocks…

…and putting a little bounce in DXY’s step.

EURUSD is contributing as it continues to decline after failing to retake its own SMA200.

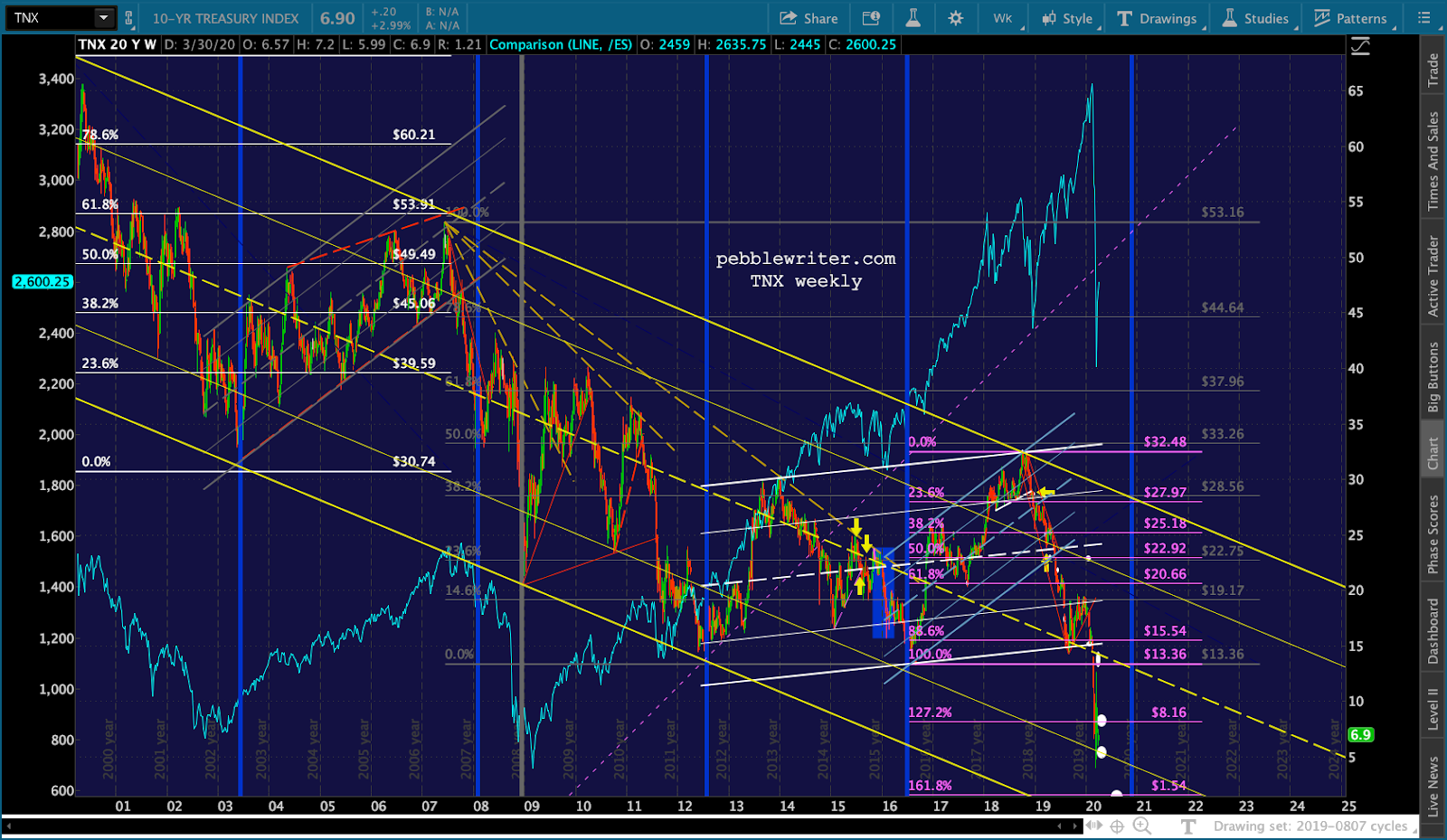

The 10Y remains below the 1.272 support…

…squeezing the 2s10s back to a neutral 47 bps...

...with the 2Y still

hanging on for dear life. A reminder, this is one of the last

substantive support levels for the 2Y. The coming breakdown will likely

widen the 2s10s, making any further equity gains difficult.

Gold continues to be a model of restraint, backtesting its red channel again as it plans another assault on 1708-1735.

Trump and Putin reportedly put their heads together yesterday to plan

a rescue for oil prices. But, CL has yet to exhibit much of a bounce

and remains mired at the lower end of our 20-26 range. Perhaps it has

something to do with all that surplus oil sloshing around, searching for any storage

facility with extra capacity.

While higher oil prices would certainly help stocks – an important

goal for many, none more so than Trump himself – they would constitute a tax on

the many unemployed/beleaguered consumers who are wondering how to

make ends meet while they await their government checks.

For many of those in high-priced areas such as major coastal towns,

of course, those checks can’t come fast enough and won’t cover

rent/mortgage payments – a topic for a future post.

Gas prices continue to loiter at the bottom of that falling channel, though the bounce off the recent lows is looking tired.

In the absence of any miraculous medical breakthroughs, it still

looks like yesterday’s highs will continue to hold and ES/SPX’s

trajectory will be lower, perhaps to the bottom of the rising purple

channels around 2350 as early as tomorrow. That should be the next

line in the sand, with ES 2155 and SPX 2138 still our next preferred

downside targets.

While we’re in forecasting mode, I’m told that this site should be

working normally sometime later today. If you’re reading this on

pebblewriter.com, you’ve already figured that out. I’ll repost on

pebblewriter.blogspot.com …just in case.

I’m going to take some time and update our COVID-19 forecast which, sadly, continues to be on target. More later.

UPDATE: 3:25 PM

As we stumble into the final hour, things aren't looking very bullish. Never underestimate the power of a last-minute VIX smackdown, but there are quite a few warning signs flashing red.

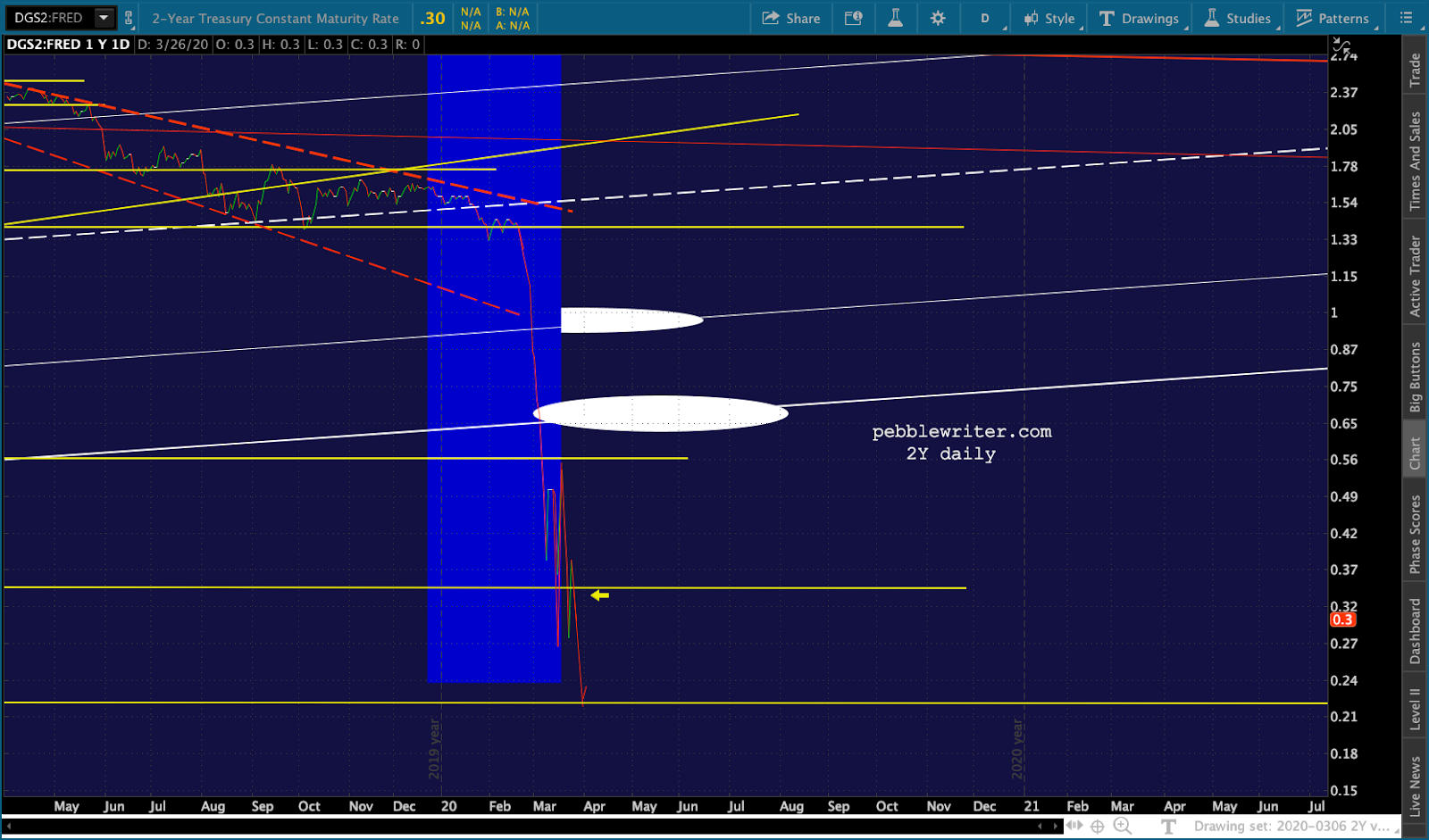

First and foremost, the 2Y just dipped down to .191, the lowest it's been since the US lost its AAA in 2011.

It quickly snapped back to the .22 support, but this is a very big deal according to our 2Y model.

The other pretty big deal continues to be the oil market collapse. Sure, it clawed its way back to the channel bottom, but for how long? The next lowest support is the Nov 2001 lows at 17.12.

Then there's DXY which, thanks to USDJPY and EURUSD, is having a hard time staying aloft.

Although the USDJPY could still go either way, the BoJ apparently hasn't signed off on a wholesale devaluation of the yen.

This leaves poor little VIX with some very heavy lifting to do. As the month- and quarter-end rebalancing winds down, can it continue to offset a very grim economic outlook which, according to Goldman, includes a -34% Q2 GPD read.

The worst of the economic data has yet to roll in, but in the days ahead we'll get ISM, EIA inventories, factory orders and payrolls. It won't be pretty.

ES and SPX - which have clearly rolled over - might be able to hold support at the close, but I wouldn't trust them overnight regardless of where they close - not on a bet.

No comments:

Post a Comment